Developing an effective organisational structure (MP3)

Developing an effective organisational structure (MP3)  Intellectual Property Office A3 ePoster Edition 13 "Intellectual property rights and entrepreneurship"

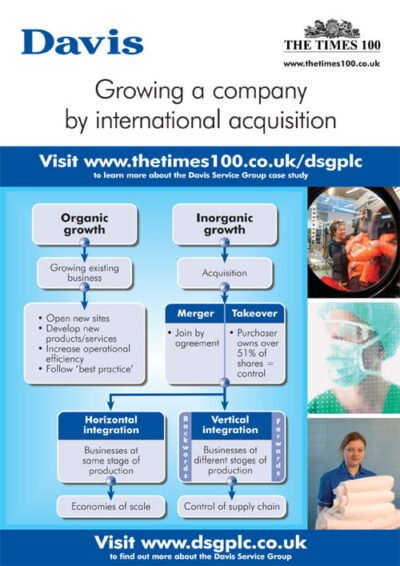

Intellectual Property Office A3 ePoster Edition 13 "Intellectual property rights and entrepreneurship"  Davis Service Group A3 ePoster Edition 13 "Growing a company by international acquisition"

Davis Service Group A3 ePoster Edition 13 "Growing a company by international acquisition"  Corporate Citizenship and the community (PDF)

Corporate Citizenship and the community (PDF)  Financial management in a retail setting (PDF)

Financial management in a retail setting (PDF)

Target costing is a pricing strategy that is used primarily in manufacturing and product development. It involves determining the desired profit margin for a product and then working backwards to establish a cost structure that allows for that profit margin while still being competitive in the market. This approach is particularly prevalent in industries where competition is fierce, and price sensitivity among consumers is high.

The essence of target costing lies in its proactive nature; rather than simply accepting costs as they arise, businesses actively seek to control and reduce costs from the outset of product development. The concept of target costing emerged in Japan during the 1960s and gained prominence in the 1980s as companies sought to improve their competitiveness in global markets. It is fundamentally different from traditional costing methods, which often focus on historical costs and may not adequately account for market conditions or consumer expectations.

By setting a target cost based on market prices and desired profit margins, companies can align their product development efforts with customer needs and market realities, ensuring that they deliver value while maintaining profitability.

Summary

- Target costing is a strategic cost management tool used to determine the maximum cost that can be incurred on a product while still earning the desired profit margin.

- Target costing is important in business as it helps in setting competitive prices, improving product quality, and enhancing overall profitability.

- The process of implementing target costing involves identifying the target cost, conducting cost analysis, and making necessary design and production changes to meet the target cost.

- Using target costing in business can lead to benefits such as improved cost management, enhanced product competitiveness, and increased customer satisfaction.

- However, there are challenges and limitations to target costing, including the difficulty in accurately predicting costs and the potential for compromising product quality to meet cost targets.

The Importance of Target Costing in Business

Target costing plays a crucial role in modern business strategy, particularly in sectors where innovation and cost efficiency are paramount. One of the primary reasons for its importance is that it encourages cross-functional collaboration within organisations. By involving various departments—such as engineering, marketing, and finance—in the target costing process, companies can foster a culture of teamwork and shared objectives.

This collaborative approach not only enhances communication but also leads to more innovative solutions for cost reduction and product design. Moreover, target costing helps businesses respond more effectively to market dynamics. In an era where consumer preferences can shift rapidly, having a clear understanding of cost structures allows companies to adapt their offerings without sacrificing quality or profitability.

For instance, if a competitor launches a similar product at a lower price point, a company employing target costing can quickly assess its own cost structure and identify areas for improvement. This agility is essential for maintaining market share and ensuring long-term sustainability.

The Process of Implementing Target Costing

Implementing target costing involves several key steps that require careful planning and execution. The first step is market research, where businesses gather data on customer preferences, competitor pricing, and overall market trends. This information is critical for establishing a realistic target price that reflects what consumers are willing to pay.

Once the target price is set, the desired profit margin is determined, which leads to the establishment of the target cost. Following this initial phase, the next step involves cross-functional teams working together to analyse the product design and production processes. This analysis aims to identify potential cost-saving opportunities without compromising quality or functionality.

Techniques such as value engineering can be employed during this stage to assess whether certain features can be modified or eliminated to reduce costs. Additionally, suppliers may be engaged early in the process to explore options for cost reductions through bulk purchasing or alternative materials.

Benefits of Using Target Costing in Business

The benefits of adopting target costing are manifold and can significantly enhance a company’s competitive edge. One of the most notable advantages is improved cost control. By establishing a target cost at the outset of product development, businesses are compelled to scrutinise every aspect of their production processes.

This scrutiny often leads to innovative solutions that not only reduce costs but also improve product quality and performance. Another significant benefit is enhanced customer satisfaction. Since target costing is inherently customer-focused, it ensures that products are designed with consumer needs in mind.

By aligning product features with what customers value most, companies can create offerings that resonate with their target audience. This alignment not only boosts sales but also fosters brand loyalty, as customers are more likely to return to brands that consistently meet their expectations.

Challenges and Limitations of Target Costing

Despite its advantages, target costing is not without its challenges and limitations. One of the primary difficulties lies in accurately estimating market conditions and consumer preferences. If a company misjudges these factors, it may set an unrealistic target price or cost structure, leading to potential financial losses.

Additionally, the dynamic nature of markets means that what may be considered an acceptable target cost today could become obsolete tomorrow. Another challenge is the potential for internal resistance to change. Implementing target costing often requires a cultural shift within an organisation, as employees may be accustomed to traditional costing methods that focus on historical data rather than forward-looking strategies.

Overcoming this resistance necessitates strong leadership and effective communication to ensure that all team members understand the benefits of target costing and are committed to its successful implementation.

Examples of Successful Implementation of Target Costing

Toyota’s Innovative Approach

One notable example is Toyota, which has long been recognised for its innovative approach to manufacturing and cost management. Toyota employs target costing as part of its lean manufacturing philosophy, allowing it to maintain high-quality standards whilst keeping costs low.

Delivering Competitive Products

By involving suppliers early in the design process and focusing on continuous improvement, Toyota has been able to deliver vehicles that meet consumer demands at competitive prices. Another example can be found in the consumer electronics industry with companies like Sony. Sony utilises target costing to ensure that its products remain appealing in a highly competitive market.

Maintaining a Leadership Position

By conducting thorough market research and engaging cross-functional teams, Sony has been able to launch products that not only meet consumer expectations but also achieve desired profit margins. This strategic approach has allowed Sony to maintain its position as a leader in innovation whilst effectively managing costs.

How Target Costing Differs from Traditional Costing Methods

Target costing stands in stark contrast to traditional costing methods, which often rely on historical data and do not take into account market conditions or consumer preferences. Traditional costing typically involves calculating costs based on past expenditures and then adding a markup for profit. This reactive approach can lead to inefficiencies and missed opportunities for cost reduction since it does not encourage proactive planning or collaboration across departments.

In contrast, target costing begins with the end goal in mind—the desired selling price based on market research—and works backwards to determine acceptable cost levels. This forward-thinking methodology fosters innovation by challenging teams to find ways to reduce costs while still delivering value to customers. Furthermore, target costing encourages ongoing assessment and adjustment throughout the product development lifecycle, ensuring that companies remain agile and responsive to changing market dynamics.

The Future of Target Costing in Business Strategy

As businesses continue to navigate an increasingly complex global landscape, the relevance of target costing is likely to grow even further. With advancements in technology and data analytics, companies now have access to more precise information regarding consumer behaviour and market trends than ever before. This wealth of data can enhance the accuracy of target costing processes, allowing organisations to set more realistic targets and make informed decisions about product development.

Moreover, as sustainability becomes a central concern for consumers and regulators alike, target costing can play a pivotal role in helping companies balance profitability with environmental responsibility. By integrating sustainability considerations into the target costing process—such as evaluating the environmental impact of materials or production methods—businesses can develop products that not only meet consumer demands but also contribute positively to society. In conclusion, as organisations strive for greater efficiency and responsiveness in their operations, target costing will likely remain a vital component of strategic planning and product development across various industries.

Its ability to align cost management with customer expectations positions it as an essential tool for businesses aiming to thrive in an ever-evolving marketplace.

Target costing is a crucial concept in the world of business, helping companies to set prices based on the desired profit margin. In a related article on businesscasestudies.co.uk, the focus is on implementing elements to earn more from Google Ads. This article provides valuable insights into maximising profits through online advertising strategies, which can be directly linked to the principles of target costing. By understanding how to optimise advertising spend and revenue generation, businesses can effectively implement target costing strategies to achieve their financial goals.

FAQs

What is target costing?

Target costing is a cost management tool used in the product development process. It involves setting a target cost for a product based on the price that customers are willing to pay, and then working to achieve that cost through design, production, and other processes.

How is target costing different from traditional costing methods?

Traditional costing methods typically involve setting a cost based on the product’s production and then adding a markup to determine the selling price. Target costing, on the other hand, starts with the desired selling price and works backwards to determine the allowable cost.

What are the benefits of using target costing?

Using target costing can help companies to design and produce products that are more cost-effective, competitive, and profitable. It also encourages cross-functional collaboration and innovation in the product development process.

What are the key steps in implementing target costing?

The key steps in implementing target costing include identifying the target selling price, determining the target cost, conducting cost analysis, and making design and production decisions to achieve the target cost.

What are some industries that commonly use target costing?

Target costing is commonly used in industries such as automotive, consumer electronics, and manufacturing, where there is intense competition and a need to continuously innovate and improve cost efficiency.