Davis Service Group is a large public limited company employing around 17,000 people. Its shares are quoted on the London Stock Exchange.

The business is based on service contracts to source, clean and maintain industrial textiles, such as protective clothing and linens. This is across four key sectors: workwear, healthcare, hotels and restaurants, and general facilities, such as washroom linen.

The company’s headquarters are in London but its operations are spread across the UK and Ireland, continental Europe and Scandinavia. These are managed by two separate companies: Sunlight in the UK and Berendsen on the Continent. Sunlight is the market leader in the UK. Berendsen is the market leader in Norway, Sweden, Denmark and Holland.

Sales for the combined group in 2008 were worth £954 million. City financial analysts have forecast that 2009 sales will be at least equivalent to the 2008 level, if not modestly ahead.

Despite the severe recession of 2008-09, Davis continued to be a profitable company. This has been the result of careful budgeting. Budgeting involves making detailed financial plans for every aspect of the business, identifying risks and ensuring that managers are committed to the outcomes that they have agreed.

Budgets are forward financial plans. They show financial targets over a given period of time for income, expenditure and cash flows within a business. Davis uses budgets to plan the future use of its resources, either in the short or long term. For example, operational areas need to assess the costs of the people needed to meet production targets or the marketing team must determine costs of promoting services to increase sales. Budgets are also communication tools which allow employees to understand where the business is heading.

This case study shows how the development and use of budgets contribute to Davis Service Group meeting its objectives.

Building a budget

A company’s objectives budget is the overall financial plan showing the expenditure of the available funds. It is driven by the aims and objectives of the organisation as well as what the organisation can actually accomplish.

Many variables in a business can be budgeted. These include:

- sales

- output

- costs operating and fixed

- profits

- cash flow

- capital investment.

The budget will be based on key assumptions about likely business conditions for the year ahead. These inform the detailed operating budgets that plan month-to-month sales, activity levels and expenditure, for example, staff costs.

Managers may need to accommodate unexpected changes with flexible budgets. For example, sales may be lower than originally expected, so the budget may need to reduce marketing expenditure and/or operational activities. An increase in orders may require additional recruitment costs for temporary staffing.

Sometimes managers use zero budgeting. This means that they must start every year from zero and justify all planned expenditure, rather than starting from the previous year’s figures. This may be appropriate for a specific, self-contained project.

In larger firms budgets are allocated for defined areas of responsibility such as:

- cost centres – sub-divisions of an organisation that are a significant source of financial cost, for example, a factory or laundry operation

- profit centres – units that contribute to the overall profits of the firm, for example, services to hotel groups.

Budgets often cover one year but may form part of a longer term plan, such as when a business is considering entering a new market. Davis Service Group’s budgetary cycle runs from January to December:

- By July/August, the financial targets for the coming year are agreed.

- In August/September, the budget is developed; accurate data is collected from the different profit centres from the new set of assumptions made for the next year.

- In October of each year, these figures and assumptions are confirmed in formal review meetings.

- By December, the full budget has been finalised at country level as well as providing the overall Group data.

Davis Service Group is careful to set budgets in consultation and not to impose them on the different parts of the business. In this way, managers at all levels feel involved in the process and are more likely to feel motivated to achieve the targets in their budgets.

Making assumptions

A budget needs to make assumptions about how internal and external business conditions will develop and change. Once the effects of these assumptions have been evaluated, managers can set forecasts for sales turnover and costs to meet profit targets. Detailed planning can then follow to estimate the plant capacity, staffing, materials and marketing needed.

Managers use sensitivity analysis to review different scenarios. They ask questions and consider the impacts of various alternatives (the “what-ifs”). For example:

The economic outlook – What is the overall economic trend for the UK and Europe? For example, increased redundancies during a recession would mean less demand for workwear. A sharp rise in the value of the euro against the British pound would make earnings from Davis” European business more valuable to the company.

Competition – What is the likely strategy of key competitors? Is there a risk of any new entrant to the market or an existing competitor leaving the market? For example, if a new competitor appeared in the market, should Davis reduce its prices (affecting its profit) or invest in additional marketing activity? Davis had to react promptly and positively in the UK when two competitors left the market in 2007-8 (one from bankruptcy and one from a strategic decision to withdraw) to take advantage of the opportunity.

Customers – How are customer needs likely to change? For example, some larger clients have been moving from simply buying a textile service to wanting a complete solution to cleanliness and safety needs. Will demand from the hospital sector grow more than that from hotels and restaurants?

Staff – Is the company recruiting sufficient staff? Are salaries high enough to keep vital knowledge and experience within the Group or does Davis need to recruit additional expertise?

Suppliers What is happening in supplier markets? For example, what will be the effect of Far East imports on prices of workwear? What is the impact of increases or reductions in utility prices (energy and water)? How will exchange rates affect costs?

Davis Service Group often constructs two or three possible scenarios so it can analyse the effects of favourable and less favourable outcomes on the business. The illustrative data below highlights the effect on profit of this approach:

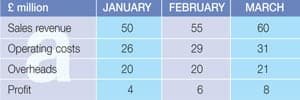

Scenario A

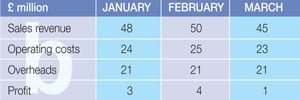

Scenario B (with new competitor)

In Scenario A. Davis increases market share and revenues. The larger volumes and relatively small increase in costs would give increased profits. In Scenario B, a competitor opens a new plant. Sales begin to fall and lower profits would result. Overheads or costs would need to be reduced to meet the gap.

Using budgets

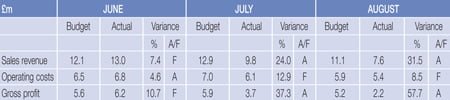

Typical budget statements are given for the Textiles budget/UK Midland region of Davis Service Group. The budget for the year (£81m) is based on the historic year data and the assumptions for the year. The two forecast outcomes use two different sets of assumptions resulting in lower or higher levels of sales.

In the example, sales for the first three months of the year were budgeted at £19.8m. Actual sales were £20.3m 2.5% above budget. If this level of increase were to continue, sales would reach £83m.

Variances may be favourable (better than expected) or adverse (worse than expected). Small variances are inevitable and usually not significant. A key task of managers is to watch for variances that are unexpected, either in their size or timing, and take action accordingly.

Managers generally focus their energy on these ‘exceptions’. For example, the weather can cause an unexpected variance for Davis Service Group’s business. June and July 2008 were warm, sunny months in the UK; the hotel and restaurant industry was busy and therefore the laundries and their staff were busy. This was followed by a wet August. The number of people going on holiday fell and resulted in reduced linen services. The knock-on effect of reduced traffic in the hotel and restaurant industry was less linen processed at Davis Service Group.

Adverse variances prompt investigation into what has gone wrong. They may suggest:

- unrealistic budgeting; budget data may need to be revised or flexed

- a failure with part of the process (e.g. missed targets by sales force); this needs immediate management attention

- a change in the external environment (e.g. a new competitor); this might require a counter-attack with an increased marketing budget.

Favourable variances represent good news but should not be ignored. Instead, they may carry an opportunity perhaps a new market is emerging or a competitor has withdrawn? Either way, managers are responsible for their budget variances and would need to report on outcomes and propose action to their own manager.

Budgets use resources so they are closely linked with key performance indicators (KPIs). KPIs help to evaluate the overall performance of the business. Davis Service Group’s KPIs include measurement of:

- organic revenue growth (i.e. sales growth excluding acquisitions)

- operational throughput (e.g. tonnage of linen processed)

- management retention rate (i.e. keeping experienced staff in the company)

- health and safety records (e.g. major incident injury rate)

- environmental performance (e.g. water and energy consumption).

As with the budget, action is prompted through variance from the KPI. For example, if a plant’s environmental performance has worsened, does it require additional investment in equipment? If health and safety incidents have increased, do employees need more training?

The benefits and drawbacks of budgeting

There are many advantages to using budgets. They:

- provide a method of allocating and using resources within the organisation

- help to monitor and control operations

- promote forward thinking

- show employees an overall picture of the direction of the organisation which can motivate staff

- help to co-ordinate different departments and align them towards shared objectives

- provide a framework for delegation.

Most importantly, budgets are an early warning system. They highlight where investigation and appropriate corrective action is necessary.

For example, Davis recognised as early as 2008 that the recession was affecting its UK linen operation. It took action to ensure the impact was managed for the second half of 2008. It then assessed the implications of recession right across the business management was put on ‘full alert’.

These benefits do not come problem-free:

- Staff time devoted to budgets carries a real opportunity cost. At Davis, 750 people are involved with budgeting. The time these workers give to the budgeting process means they are not available to carry out other responsibilities.

- Errors and inaccuracies will always remain since it is impossible to predict the future. Major external events such as rising energy prices or the global recession may distort the whole process.

- Budgets involve and affect people, they may cause conflict. There may be difficult choices over where limited funds are spent. Some departments with tight budgets could feel constrained. This carries the risk of frustrating initiative and enterprise.

Conclusion

Davis operates across 15 countries and has a sales turnover of over £1 billion. To meet its needs, the company has developed a robust and detailed budgeting and planning process involving its managers. Budgeting provides an essential forecasting, control and feedback system on which effective management depends. This process translates competitive strategy into reality.

Evidence of the power of managed budgeting was seen as recession gripped the European economies in 2008. Davis was able to assess effects and build new and realistic assumptions into its budgets for the remainder of 2008 and 2009. These have proved resilient in practice. As an exceptionally challenging year ended, the company was on track to fulfil budget expectations.

By identifying and managing risks, Davis Service Group has been able to return profits, dividends and cash flow for shareholders in a difficult economic climate. This also allows the business to invest for growth in 2010 and beyond.