What is a budget?

A budget is a financial plan that sets out, using figures, an organisation’s expected future results. For planning purposes, organisations can use many different types of budgets. For example:

- Income and expenditure budgets. These show how much an organisation expects to receive and to spend in future periods.

- Production budgets. These set out how much an organisation must produce in coming periods of time in order to meet demand.

- Profit budgets. These bring together planned sales, costs, and profit figures.

By creating budgets, managers can:

- set out a clear plan, involving target figures for defined periods of time

- communicate their targets clearly

- motivate employees to achieve these targets

- control performance by monitoring actual outcomes against planned targets

- meet the organisation’s objectives.

This case study illustrates how Kraft Foods uses budgets to enable it to meet business objectives related to financial performance with a view to achieving its vision: to become ‘the undisputed global food leader.‘

Kraft has several important objectives related to its vision. These include:

- being the employer of choice

- being a food industry high performer

- becoming an indispensable partner to customers

- being a responsible organisation and a positive force in the communities in which Kraft employees live, work and make its products

- remain focused and innovative.

Budgets help Kraft to meet these objectives in a planned forward-thinking way.

Budgets are created through consultation with all areas of the business, to achieve a shared understanding about objectives for the future visions of their teams. The Finance team supports and contributes to the work generated by other business functions to build and secure their support for the budget.

To be effective Kraft recognises that a budget must be challenging but also realistic, so that people feel it can be achieved and is worth working towards. One important element is to identify cost savings that can be re-invested to continue to grow Kraft’s powerbrands and to develop its people. Reducing costs by eliminating waste is vital in the modern food industry which is driven by price competition and consolidation in the retail sector.

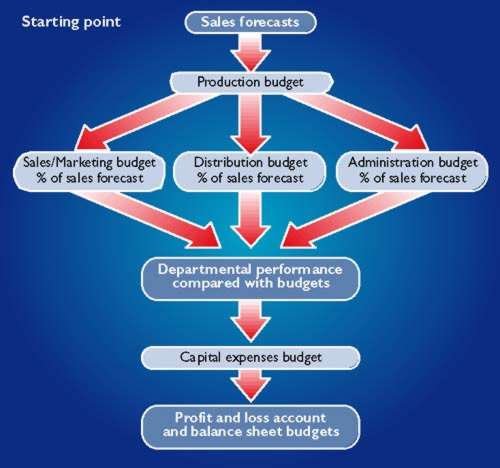

Kraft´s income and expenses budget

A typical budget:

- relates to a defined time period (usually twelve months)

- is designed and approved well in advance of the period to which it relates

- shows expected income and expenditure – income is the amount of money a business receives from its sales.

- includes all capital expenses likely to be incurred in furthering the organisation’s objectives – expenses are the costs incurred in order to make those sales.

To help control expenditure the Finance team collates the costs of the business in relevant groups called cost centres, so that analysis can be meaningful and also well controlled by those directly responsible for authorising the spend.

Many companies, including Kraft, use cost centres that relate to particular factories or production units. Within Kraft each manager is assigned clear responsibility for governing the costs which are allocated to his/her cost centre.

The budgeting process enables Kraft to make clear plans for individual cost centres, which build the budget for the whole organisation. The whole purpose of this exercise is to quantify the likely future costs of the whole operation, whilst always maintaining focus on the future plans for the company.

Kraft sells its wide portfolio of products to a variety of different customers; ranging from the corner shop, to the cash and carry and large multinational supermarket chains. In doing so, it incurs:

- raw material costs and production costs to manufacture the products to sell

- marketing expenses associated with any promotional activity including media advertising

- selling expenses involved in selling its goods into supermarkets and other customers

- distribution expenses when transporting the products from its European and UK factories to the customer.

The starting point for building a budget is to forecast the likely sales based on historical information in conjunction with Kraft’s and third party understanding of the business environment. This indicates what quantities of products need to be produced and the timing of manufacture.

With these figures in place, budgets can then be allocated for costs relating to sales, marketing and administration, and figures established for the likely costs of storing and transporting the goods (i.e. distribution). These details provide data for relevant departments (e.g. sales, administration etc). Figures can then be inserted for likely capital expenses. The final stage is to construct a budgeted profit and loss account and balance sheet.

Once the budget has been set and agreed by the management teams within Kraft, it becomes the mechanism through which managers monitor progress on a particular business component (for example, a brand, or factory) or on total company performance.

The importance of feedback

The budgeting process is a cycle of ongoing review and monitoring. Every month, Kraft uses variance analysis to identify deviations within the monthly result. A variance is the difference between the budgeted figure and the actual figure.

Variances can be favourable or adverse. For example, if actual sales income was greater than budget, this would be a favourable variance. On the other hand, if actual expenses were greater than budget, this would be an adverse variance.

By monitoring performance monthly, it is possible to alert cost centre managers to variances so that they can take appropriate corrective action or justify the new level of spend. At all stages the Senior Management team of Kraft is fully aware of any material variances that are derived from comparing actual spend vs budgeted figures.

Periodic reviews which are organised by the Budget Accountant, allow there to be a forum within which any feedback can be given on current actual spend vs plan, ensure that it is possible to reforecast the plan or alter current activity.

- Single loop feedback involves making correction to current activities in order to ‘get back on course’.

- Double loop feedback involves amending the original plans so that they more accurately reflect current business reality.

In a company like Kraft, this ability to amend the budget is an important aspect of management. Kraft’s operating environment is subject to rapid change, for example, in consumer demand patterns, in production technology, in competitor activity. So Kraft has to remain flexible and ready to respond to any challenges that it faces. Any one budget may be altered a number of times during a year, although there would always be a considered reason for doing so.

Constructing an expense budget

Each cost centre budget is seen as part of an overall plan designed to meet company objectives. Constructing cost centres’ individual budgets involves detailed consultation about company objectives, marketing objectives and relevant income and expense projections. These can be brought into line and match changes in the external business environment.

Using this as a basis it is a reasonably straightforward exercise to calculate other expenses, including the number of people (and their remuneration packages, such as pension expenses, national insurance, travel costs) required to run a particular part of the business.

In the modern business world the rate of change is such that it is impossible to have a clear picture of the future. Inevitably it takes time to build the ‘big picture’ from lots of small, shifting scenarios relating to individual cost centre budgets. Budgeting may be difficult, but it is essential for a business to stay in control and ‘ahead of the game’.

Advantages and disadvantages of expense budgeting

Budgeting provides organisations with detailed analysis of future and current proposed spending patterns, enabling much better control (by responding to variances). Performance can be analysed quantitatively (in numbers), making it possible to measure financial success. Measurement of results can serve as a motivational tool for many employees.

Budget analysis also makes it possible to identify unnecessary costs that can be removed so as to focus funds on value adding activities. Kraft uses budgetary control to remain focused on the hard (quantitative) and soft (qualitative) benefits of re-distributing spend.

However, it is important to keep sight of the organisation’s long term goals to avoid the risk that budgeting might lead to short-term focus on financial results. This could foster cost cutting exercises at the expense of strategy. In the worst case, individual managers may pursue exclusively their own narrow goals rather than business wide ones.

If individual managers are not happy with the budget they may co-operate poorly, so it is important to have detailed discussions to achieve collective agreement. This is why Kraft as an organisation retains a consultative approach to constructing budgets.

Alternative types of budgeting

There are a number of budgeting types to choose from. Kraft uses a mix of the following.

i. Zero based budgeting

In a dynamic business it often makes sense to ‘start afresh’ when developing a budget rather than basing ideas too much on past performance. This is appropriate to Kraft because the organisation is continually seeking to innovate. Each budget is therefore constructed without much reference to previous budgets. In this way, change is built into budget thinking.

ii. Strategic budgeting

This involves identifying new, emerging opportunities, and then building plans to take full advantage of them. This is closely related to zero based budgeting and helps Kraft to concentrate on gaining competitive advantage.

iii. Rolling budgets

Given the speed of change and general uncertainty in the external environment, shareholders seek quick results. US companies typically report to shareholders every three months, compared with six months in the UK. Rolling budgets involve evaluating the previous twelve months’ performance on an ongoing basis, and forecasting the next three months’ performance.

iv. Activity based budgeting

This examines individual activities and assesses the strength of their contribution to company success. They can then be ranked and prioritised, and be assigned appropriate budgets.

Conclusion

The world food market is dynamic and highly competitive. To succeed, Kraft recognises the need to build in flexibility that enables it to seize appropriate opportunities into its planning activities.

Kraft’s budgeting process is based on consensus and shared understandings. By using rigorous but flexible budgeting arrangements the various components of Kraft are best able to contribute in a coordinated way to delivering strategic objectives.

Kraft Foods UK | Budgeting and strategy