Regeneration: meeting needs in a changing environment (PDF)

Regeneration: meeting needs in a changing environment (PDF)  Managing external influences (PDF)

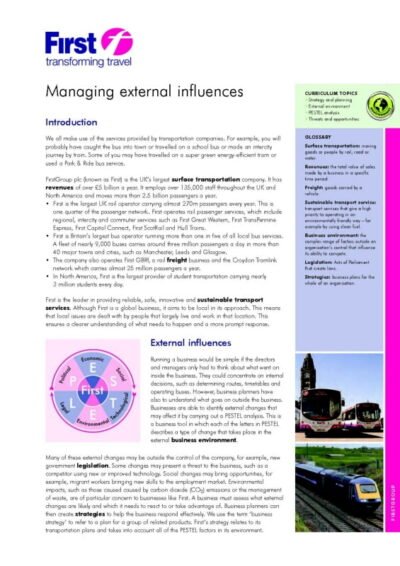

Managing external influences (PDF)

Costs are a fundamental aspect of business operations, and comprehending the various types of costs is vital for effective financial management. Businesses encounter several cost categories, including fixed, variable, direct, indirect, and semi-variable costs. Fixed costs remain constant regardless of production or sales levels, encompassing expenses such as rent, salaries, insurance, and depreciation.

Variable costs, conversely, fluctuate with production or sales volumes, including raw materials, direct labor, and sales commissions. Direct costs are expenses directly attributable to a specific product or service, such as materials and labor costs. Indirect costs, also termed overhead costs, cannot be directly linked to a particular product or service and include utilities, administrative salaries, and office supplies.

Semi-variable costs possess both fixed and variable components, exemplified by utilities with a fixed basic charge and a variable usage charge. Comprehending these cost categories is crucial for businesses to make informed financial decisions. Through cost analysis and categorization, companies can more effectively allocate resources, establish pricing strategies, and make strategic decisions to enhance profitability.

Key Takeaways

- Understanding the different types of costs is essential for effective cost management, including fixed costs, variable costs, direct costs, and indirect costs.

- Factors affecting costs include market conditions, competition, technology, and government regulations, which can impact pricing and expenses.

- Managing and controlling costs involves setting clear cost targets, monitoring expenses, and implementing cost-saving measures to improve profitability.

- Hidden costs to consider include opportunity costs, intangible costs, and costs associated with poor quality, which can impact the overall financial health of a business.

- Calculating and budgeting costs requires accurate forecasting, tracking expenses, and creating a realistic budget to ensure financial stability and growth.

Factors Affecting Costs

Factors Affecting Costs

Economies of scale refer to the cost advantages that businesses can achieve as a result of increasing their scale of production. As production levels increase, the average cost per unit decreases, leading to lower overall production costs. This can result in higher profitability for businesses.

The Impact of Technology

Technology also plays a significant role in affecting costs. Advancements in technology can lead to increased efficiency and productivity, reducing production costs. Automation and digitalization can streamline processes and reduce labor costs, while also improving quality and consistency.

Competition and Government Regulations

Competition in the market can also impact costs. Intense competition can lead to price wars and pressure on profit margins, forcing businesses to find ways to reduce costs in order to remain competitive. This can lead to cost-cutting measures and efficiency improvements to maintain profitability. Government regulations and policies can also affect costs for businesses. Compliance with regulations may require additional resources and expenses, such as environmental regulations or labor laws. Changes in tax laws or tariffs can also impact production costs and overall business expenses.

By understanding these factors affecting costs, businesses can better anticipate and respond to changes in their operating environment. This can help them make informed decisions to manage and control costs effectively.

Managing and Controlling Costs

Managing and controlling costs is essential for businesses to maintain profitability and sustainability. There are several strategies that businesses can employ to effectively manage and control their costs, including cost analysis, budgeting, cost reduction initiatives, and performance monitoring. Cost analysis involves examining all aspects of a business’s operations to identify areas where costs can be reduced or eliminated.

This may involve conducting a thorough review of all expenses, including fixed and variable costs, direct and indirect costs, and semi-variable costs. By analyzing these costs, businesses can identify opportunities for cost savings and efficiency improvements. Budgeting is another important tool for managing and controlling costs.

By creating a detailed budget that outlines expected revenues and expenses, businesses can set targets for cost control and monitor their financial performance against these targets. Budgeting helps businesses allocate resources effectively and identify areas where costs may be exceeding expectations. Cost reduction initiatives involve implementing strategies to reduce expenses without sacrificing quality or productivity.

This may involve renegotiating contracts with suppliers, streamlining processes to improve efficiency, or investing in technology to automate tasks and reduce labor costs. By identifying areas where costs can be reduced without compromising value, businesses can improve their bottom line. Performance monitoring is crucial for evaluating the effectiveness of cost management strategies.

By regularly monitoring key performance indicators related to costs, such as cost per unit produced or cost per customer acquired, businesses can identify trends and make adjustments as needed to achieve their cost management goals. By employing these strategies for managing and controlling costs, businesses can improve their financial performance and competitiveness in the market. Managing and controlling costs is essential for businesses to maintain profitability and sustainability.

There are several strategies that businesses can employ to effectively manage and control their costs, including cost analysis, budgeting, cost reduction initiatives, and performance monitoring. Cost analysis involves examining all aspects of a business’s operations to identify areas where costs can be reduced or eliminated. This may involve conducting a thorough review of all expenses, including fixed and variable costs, direct and indirect costs, and semi-variable costs.

By analyzing these costs, businesses can identify opportunities for cost savings and efficiency improvements. Budgeting is another important tool for managing and controlling costs. By creating a detailed budget that outlines expected revenues and expenses, businesses can set targets for cost control and monitor their financial performance against these targets.

Budgeting helps businesses allocate resources effectively and identify areas where costs may be exceeding expectations. Cost reduction initiatives involve implementing strategies to reduce expenses without sacrificing quality or productivity. This may involve renegotiating contracts with suppliers, streamlining processes to improve efficiency, or investing in technology to automate tasks and reduce labor costs.

By identifying areas where costs can be reduced without compromising value, businesses can improve their bottom line. Performance monitoring is crucial for evaluating the effectiveness of cost management strategies. By regularly monitoring key performance indicators related to costs, such as cost per unit produced or cost per customer acquired, businesses can identify trends and make adjustments as needed to achieve their cost management goals.

By employing these strategies for managing and controlling costs, businesses can improve their financial performance and competitiveness in the market.

Hidden Costs to Consider

In addition to the more obvious direct and indirect costs that businesses incur, there are also hidden costs that should be considered when managing finances. These hidden costs may not be immediately apparent but can have a significant impact on a business’s bottom line if left unaddressed. One common hidden cost is employee turnover.

The cost of recruiting, hiring, training, and onboarding new employees can add up quickly. Additionally, there may be productivity losses during the transition period as new employees get up to speed in their roles. Businesses should consider investing in employee retention strategies to minimize turnover-related expenses.

Another hidden cost is poor quality or defective products. The cost of rework or replacing faulty products can impact production efficiency and customer satisfaction. Investing in quality control measures and continuous improvement initiatives can help reduce these hidden expenses.

Inventory carrying costs are another often overlooked expense. Holding excess inventory ties up capital that could be used elsewhere in the business. Additionally, there are storage and insurance expenses associated with maintaining inventory levels.

Businesses should strive to optimize their inventory management practices to minimize carrying costs. Finally, there are hidden opportunity costs associated with missed opportunities or underutilized resources. For example, if a business fails to capitalize on a new market trend or does not fully leverage its existing assets, there may be missed revenue potential.

Businesses should regularly assess their operations to identify areas where they may be leaving money on the table. By considering these hidden costs in addition to more visible expenses, businesses can take a more comprehensive approach to managing their finances and improving their overall profitability. In addition to the more obvious direct and indirect costs that businesses incur, there are also hidden costs that should be considered when managing finances.

These hidden costs may not be immediately apparent but can have a significant impact on a business’s bottom line if left unaddressed. One common hidden cost is employee turnover. The cost of recruiting, hiring, training, and onboarding new employees can add up quickly.

Additionally, there may be productivity losses during the transition period as new employees get up to speed in their roles. Businesses should consider investing in employee retention strategies to minimize turnover-related expenses. Another hidden cost is poor quality or defective products.

The cost of rework or replacing faulty products can impact production efficiency and customer satisfaction. Investing in quality control measures and continuous improvement initiatives can help reduce these hidden expenses. Inventory carrying costs are another often overlooked expense.

Holding excess inventory ties up capital that could be used elsewhere in the business. Additionally, there are storage and insurance expenses associated with maintaining inventory levels. Businesses should strive to optimize their inventory management practices to minimize carrying costs.

Finally, there are hidden opportunity costs associated with missed opportunities or underutilized resources. For example, if a business fails to capitalize on a new market trend or does not fully leverage its existing assets, there may be missed revenue potential. Businesses should regularly assess their operations to identify areas where they may be leaving money on the table.

By considering these hidden costs in addition to more visible expenses, businesses can take a more comprehensive approach to managing their finances and improving their overall profitability.

Calculating and Budgeting Costs

Calculating and budgeting for costs is an essential aspect of financial management for businesses. By accurately estimating expenses and setting budgets accordingly, businesses can better plan for future financial needs and make informed decisions about resource allocation. To calculate total production or service delivery cost per unit produced or delivered (cost per unit), businesses must consider both fixed and variable expenses associated with production or service delivery.

Fixed expenses such as rent or salaries are divided by the number of units produced or delivered over a specific period to determine the fixed cost per unit. Variable expenses such as raw materials or direct labor are totaled for the period then divided by the number of units produced or delivered over the same period to determine the variable cost per unit. Budgeting involves setting targets for expected revenues and expenses over a specific period based on historical data or projected trends.

By creating detailed budgets for different aspects of the business such as sales, marketing, operations, and administration, businesses can establish financial goals and allocate resources accordingly. It’s important for businesses to regularly review their budgets against actual performance to identify any discrepancies or areas where adjustments may be needed. By continuously monitoring their financial performance against budgeted targets, businesses can make informed decisions about resource allocation and identify opportunities for cost savings or revenue growth.

By accurately calculating production or service delivery cost per unit produced or delivered (cost per unit) as well as setting detailed budgets based on historical data or projected trends then regularly reviewing actual performance against budgeted targets; businesses can better plan for future financial needs while making informed decisions about resource allocation. Calculating and budgeting for costs is an essential aspect of financial management for businesses. By accurately estimating expenses and setting budgets accordingly; businesses can better plan for future financial needs while making informed decisions about resource allocation.

To calculate total production or service delivery cost per unit produced or delivered (cost per unit), businesses must consider both fixed and variable expenses associated with production or service delivery; Fixed expenses such as rent or salaries are divided by the number of units produced or delivered over a specific period; Variable expenses such as raw materials or direct labor are totaled for the period then divided by the number of units produced or delivered over the same period; Budgeting involves setting targets for expected revenues & expenses over a specific period based on historical data or projected trends; By creating detailed budgets for different aspects of the business such as sales; marketing; operations; administration; businesses can establish financial goals & allocate resources accordingly; It’s important for businesses to regularly review their budgets against actual performance; By continuously monitoring their financial performance against budgeted targets; Businesses can make informed decisions about resource allocation & identify opportunities for cost savings or revenue growth;

Strategies for Reducing Costs

Reducing operational expenses is a key focus area for many businesses looking to improve profitability. There are several strategies that businesses can employ to reduce their operating costs without sacrificing quality or productivity. One strategy is to negotiate with suppliers for better pricing terms or seek alternative suppliers who offer more competitive rates without compromising on quality.

By leveraging purchasing power through bulk buying or long-term contracts with suppliers; Businesses may be able to secure discounts & reduce procurement expenses; Another strategy is to invest in technology & automation; which can streamline processes & reduce labor requirements; leading to lower production & operational expenses; Additionally; technology investments may improve overall efficiency & quality; Outsourcing non-core functions such as accounting; IT support; customer service; & manufacturing; allows businesses to focus on their core competencies while reducing overhead & labor expenses; Implementing energy-saving measures & sustainable practices not only reduces utility bills but also demonstrates corporate social responsibility; Finally; implementing lean management principles & continuous improvement initiatives

If you are interested in learning more about the costs associated with running a business, you may want to check out the case study on Securicor. This article discusses how the company manages its costs and the impact it has on its overall performance. You can find the case study here.

FAQs

What are costs?

Costs are the expenses incurred in the process of producing goods or services. These expenses can include raw materials, labor, overhead, and other factors.

What are the different types of costs?

There are various types of costs, including fixed costs, variable costs, direct costs, indirect costs, and opportunity costs. Each type of cost plays a different role in the overall financial picture of a business.

How do costs impact businesses?

Costs have a direct impact on a business’s profitability and overall financial health. Managing costs effectively is crucial for businesses to remain competitive and sustainable in the long term.

What are some strategies for managing costs?

Businesses can manage costs by implementing strategies such as cost reduction, cost control, cost allocation, and cost-benefit analysis. These strategies help businesses optimize their spending and improve their financial performance.

How do costs affect pricing?

Costs play a significant role in determining the pricing of goods and services. Businesses need to consider their production costs when setting prices to ensure they are able to cover expenses and generate a profit.

What are some common challenges related to costs?

Common challenges related to costs include cost overruns, cost fluctuations, and cost inefficiencies. These challenges can impact a business’s financial stability and require proactive management to address.