Let’s face it. Many businesses fail within the first year. A staggering 18.4% of businesses don’t make it less than 12 months after they open. After two years, that number increased to 30.6%.

Then there are the lucky ones or the 10% of start-ups that succeed. According to research, there’s an 18% success rate for first-time start-up founders.

Whichever category you belong to, you might decide to implement a business exit strategy either to cut your losses if the company is failing or maximize your profits if your company is booming. An exit strategy is a contingency plan used by a business owner to reduce or liquidate their company ownership if it fails. It can also determine how the owner can make a significant profit from the sale of the company if it attracts the attention of another investor.

In this article, you’ll learn how to implement a business exit strategy:

1. Get Your Financial Documents in Order

When you decide to exit the business, you will need to get all the necessary financial documents in order. Financial documents describe the commercial activities, predetermined criteria, and financial performance of a company. They can be income statements, balance sheets, and cash flow statements, among others.

You can use these financial documents to help you decide the best exit strategy to take. Plus, you’ll have to turn over these financial documents to the person you’re selling a controlling stake of your business to or your entire business to, should you decide to sell. This way, they can understand the company’s financial situation and craft their own business strategies after their purchase.

To ensure a smooth turnover of financial documents in the event you decide to exit the company, make sure they are constantly updated from the first day you start running the business. You never know when you decide to opt-out, after all.

2. Think Closely about Your Possibilities: Closing vs. Selling

Once you have a good idea of your company’s financial health, you can now weigh your different options for exiting.

When your growth model fails or becomes too successful for its own good, you may choose to close or sell your business. Closing your business means that you would have to shut your operations entirely. It also means selling all the assets you can make money off and losing the clients and business relationships built during the coarsening.

If your business isn’t profitable and might be running in losses, liquidation resources as a business exit strategy can be the best resort. It is a simple strategy that will allow you to pay off your creditors and reduce your financial burden.

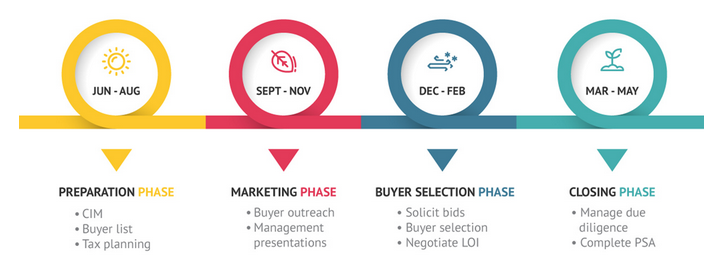

However, selling or closing a business may take up to a year. You should divide the business process into four distinct phases: preparation, marketing, buyer selection, and closure.

Selling your business to a new owner with whom you are familiar with is a simple, fast approach to exit the business. It could be family-owned businesses or friends who you think would carry on with your legacy. In an ideal situation, you may find someone who shares your passion and is willing to lead.

Another option would be to sell the business to someone from the existing employees, management, or investors. They would have a simple time taking over since they are aware of the obstacles and possibilities, making them a capable competitor.

A merger might be a good alternative if you wish to stay actively involved in the firm. It allows you to hold a managerial position in the merged company. But if you don’t want any involvement, a cash and stock purchase is the way to go. You can also make an initial public offering, which allows a private company to sell its stock to the general public on the stock exchange. It also may allow your early investors to cash out their investments.

However, you need to study the current market worth of your company and what buyers are willing to pay now. Working with a valuation expert, business broker, or investment banker can help you determine your options.

3. Work with Your Existing Investors

Regardless of your type of business, you must work with your existing investors when you decide to opt-out. You should keep them in the loop about your business exit strategy plans to avoid financial or legal complications. Your investors made it possible for your business to exist in the first place. It is only fair to keep them updated if you shut down or hand over the reins of your company to someone else.

If you’re closing down your company, you should negotiate the money owed to your investors with the earnings from the sale of your company.

If you opt to sell your stake in the company, you should give the new owner all the relevant information about the company’s existing investors.

Also, provide these current investors with sufficient information on the new owner. You can create a comprehensive report about everything they need to know. If you don’t have time to write, use artificial intelligence tools. A guide to generative AI can help you make the most out of these time-saving tools. If investors are satisfied with the new owner’s abilities based on your report, they may opt not to withdraw money from the business.

4. Inform Your Employees

You’ll need to communicate your business exit plans to your staff.

If you decide to shut down the company, explain to them the severance package they’re entitled to. Be clear about how you could help them as well. Maybe you’ll write recommendation letters, and call people to introduce them to future employment opportunities, among other things.

If you decide to sell your stake, tell them who’s taking over. So, if they have concerns about the firm’s future direction or the corporate culture which may both change because of your departure they can decide to leave as well.

Here are a few other actionable tips we suggest:

- Tell them before announcing it to the media.

- Announce it in a meeting. It’s more personal and respectful to do so than sending an email.

- Be transparent. Will there be any layoffs or salary reductions, or will they be able to keep their jobs? Your employees will understandably ask a lot of questions, and you need to be able to answer them promptly and honestly.

Always remember that your employees are people with emotions who will be affected by your business decision. Give them the transparency they deserve every step of the way.

5. Notify Your Clients

Your clients also deserve to know your business exit strategy plans. Their support is also what led to the continuity of your operations, after all.

But you need to strategically time your announcement as you may be waiting on some outstanding payments. You wouldn’t want some unscrupulous clients to take the news of your closing operations as a way to get out of paying their dues.

If you decide to sell your stake, you could introduce your clients to the new owner and management. Say you’re closing the business for good. It’s always still a kind act to point your clients towards sources that could be your replacement.

Your customers are the ones who drive revenue. So, you must always be thankful to them. Building a genuine connection takes time and work, which means you shouldn’t just throw away these customer relationships if you opt-out. They might even give you the support you need if you decide to start a new company in the future.

6. Ensure Seamless Transition to New Owner (for Business Sale)

You need to ensure a seamless transition should you decide to sell your stake. The transition period after your sale is something you can’t avoid. In fact, the details of this transition will likely crop up in your negotiations with a potential new buyer.

When you present a detailed plan for how you plan to support the new owner post-purchase, you boost buyer confidence. After all, you give them the impression that you won’t leave them to adapt as the new owner on their own. Coupled with professional PR services that can help boost your company’s image, a detailed transition plan can also help you in company valuation. You might be able to sell your stake at a higher price since you give the new buyer the assurance that their huge investment is protected.

There are three stages to consider to ensure a seamless transition to the new company owner.

In the training stage, you, as the seller, should run through your list of do’s and don’ts with your buyer. Show them how a typical day in the business starts and finishes. Go around each department. Explain to them the relevant processes followed in each department to ensure overall business operations run smoothly. Here are some of the other things you should inform them about:

- People you make contact with for work-related matters

- Payroll management

- Routine company maintenance tasks

Answer any questions the new owner might have as you introduce them to the ins and outs of the business. Your goal is to put them in a position to be successful in running the business in the near future.

You’ll have to gradually take a hands-off approach to running business operations once you see the buyer adjusting little by little as the new owner. So, as you enter the handover stage, the new owner should be running at least 75% of the company’s operations.

The new buyer should be making some of the crucial business decisions at this point. The company’s customers and employees should have, by now, also established relationships with the new owner. At this stage, though, you still need to be on hand to answer any other questions the new owner may have.

Once the new owner runs the company’s operations 100%, you enter the final stage of the transition or the assistance stage. Although at this stage you’re no longer directly involved in running any aspect of the company’s operations, you should still be available to answer any queries by the new owner. Communication between the old and new owner at this stage is usually done via phone or email. If you opt for this second option, though, make sure you use an email finder to ensure your emails reach the intended recipient.

The assistance stage can’t go on forever, though. Note that you and the buyer should have decided on how long you can be on hand to give them the necessary support post-purchase.

When you sell something as big as a company, you can’t just go and leave everything to the new owner after the purchase. It’s your responsibility to ensure they can succeed in their new role. This is a great way to ensure good business relationships as well. That can come in handy should you decide to give it a go as an entrepreneur once again.

Bottom Line

Exiting the business is always an option for company owners like you. Sometimes, things just don’t go as planned and it’s just better to move on to a more suitable path. Other times, things go so smoothly that the more prudent business decision would be to sell to maximize profit.

But whether you’re shutting down your business for good or selling your stake to someone else, you need a plan.

You learned how to implement a business exit strategy with this article.

Get your finances in order so you can understand your choices before choosing how to opt-out. Based on that, choose the best way to exit the business. Then work with your existing investors, and inform your employees and clients, too. If you’re selling your stake, ensure a seamless transition to the new owner.

Implementing a business exit strategy requires a well-thought-out plan for your growth and the future of people involved in this process. So, give yourself time to build your exit strategy.