Investment decisions involve weighing up the risk and the likely rewards of various options. It is often the riskiest alternatives that yield the highest possible gains while the least risky options may yield smaller rewards.

Business decision makers therefore have to weigh up risk so as to provide the most suitable rewards for stakeholders including shareholders and customers. The starting point is a company’s overall aim which then filters down into a strategy, creating a balanced portfolio made up of numerous investments.

This case study examines the processes involved in weighing up risks in order to create a balanced portfolio at BG Group, one of the leading energy businesses in the UK. The Case Study illustrates typical stages involved in deciding whether to bid for the right to explore for and develop new gas fields and, importantly, how much to bid.

Before weighing up the risks, ethics are an integral part of BG Group’s considerations – i.e. making morally correct decisions, whether these be concerned with environmental issues, health and safety or any other decision involving the difference between ‘right and wrong’ behaviour. In other words the ‘best’ investment decision will balance economic, social and environmental considerations.

More than just finance

Ethical decisions are integral in making investment decisions. BG Group’s Statement of Business Principles sets out the fundamental values and ethical principles within which the Company operates. BG Group will only enter countries where the Company can operate in accordance with its Business Principles.

The following example gives an outline of the important statistical and financial procedures involved in making an investment decision. However, it is important to emphasise the weight given to non-financial factors involved in decision making. Gas is the cleanest fossil fuel, but any form of energy production involves some form of environmental cost, e.g. the sight of windfarms located in fields, or harmful release of greenhouse gases when burning fossil fuels.

BG Group will only bid to explore if it can operate within its ethical guidelines. The Company always seeks to apply its Business Principles. This can sometimes be difficult since natural gas resources are found in countries at different stages of economic, environmental, political and social development.

BG Group

The gas industry is today in the private and public sector and there are a number of companies competing in the industry. Some of these companies are government owned. Others are owned by private shareholders who appoint directors to represent their interest. The directors appoint professional managers to run the business. Like electricity and telecommunications, gas is a ‘network industry’. In the case of gas, consumers are linked to a central network of gas pipelines.

BG Group is an integrated business in that it has activities across the whole range of gas operations, from the reservoir to the customer. BG Group’s exploration and production (E&P) business finds and develops gas reserves.

Natural gas is delivered to customers either by BG Group’s transmission and distribution (T&D) business using pipelines or by the liquefied natural gas (LNG) business via LNG ships. BG Group’s power business focuses on the creation of electricity by natural gas-fired power generation plants. The illustration shows the gas chain indicating the various links in an integrated business involved in bringing gas to final consumers.

Demand for gas is projected to grow at an increasing rate over the next decade, outstripping the growth in demand for other major sources of energy. As an energy source, gas is a relatively clean fossil fuel, abundant and is increasingly becoming the fuel of choice for consumers, on both environmental and economic grounds.

Field development

The gas business has a number of characteristics that are particularly important in relation to investment decision making:

- It is very capital intensive so decisions may typically involve a spend of several hundred million pounds.

- There are long lead times between the start of a project and the receipt of earnings from that project, typically over five years from first investment to first revenue.

- The taxation and contract structure is unique to the energy industry and is complex. Gas is a finite resource for a nation. Its exploitation is of strategic importance to the host government for some time.

Governments own the rights to minerals found on land (onshore) and underwater (offshore) in their countries. Governments divide the ground into exploration ‘blocks’ and invite energy companies to bid for the right to explore for oil and gas in those blocks.

To earn the right to explore a block, the energy company commits to a work programme, which describes the steps it will take in order to find oil/gas. The energy company’s investment and expertise helps governments access the mineral wealth beneath the ground. BG Group makes important decisions as to whether or not to apply for the right to explore for new gas fields and how much to bid.

Key risks

Shown below are some of the key risks in a typical gas project and the experts responsible for addressing those risks:

- geologists and geophysicists evaluate the risks around volume and the chance of finding those volumes

- engineers examine facility and well design, costs, production rates

- HSSE managers assess health, safety, security and environmental risks

- economists analyse market demand and price, government and partner commercial terms.

Investment appraisal

Discounted cash flow is an important technique for investment appraisal. The discounted cash flow approach is a way of valuing the future returns on investment by assessing the values of these returns in terms of their value today. It places emphasis on the cost of funds tied up in a project by considering the timing of cash flows.

For example, we all instinctively know that £1 in the hand today is worth more than a promise of £1 in the future. This is because:

- Inflation may lower the real value of money.

- The money cannot be put to constructive use in the meantime (i.e. earning interest in the bank or applied to another project).

- There is always the risk that unforeseen circumstances will prevent you from receiving the amount you have been promised.

Appraising investments using the discounted cashflow method allows the Company to undertake a capital allocation process, which involves ranking projects and selecting those that add the most value to the Company. It therefore incurs the opportunity cost of those projects that add value but cannot be financed as sufficient funds are not available to undertake them.

Ultimately, the value of any investment is the present value of the future free cash flows – Net Present Value (NPV)- that the investment is expected to generate. Therefore, it is necessary to forecast the economic cashflows and discount them appropriately to allow for the fact that they will not be received until some time in the future. BG Group uses a discount rate that reflects the return its investors (shareholders and banks) expect for investing in a non risk free activity (compared to depositing money in a bank account).

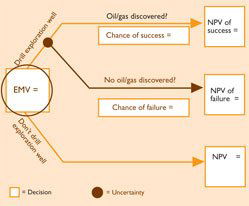

The NPV calculation always assumes the project is a success. However, there is a chance that no oil or gas is present (geological risk), this risk must therefore be reflected in the valuation. This is achieved by assigning probabilities to the values of successful and unsuccessful outcomes. The sum of these risked values is the Expected Monetary Value (EMV).

The EMV calculation can be illustrated by a decision tree. Decision trees are a simple way of choosing from alternative courses of action when faced with uncertainty. The basic procedure for constructing a decision tree is to set out a series of alternative branches of the tree and then to calculate the probability of the event occurring and the likely money value of the return.

In a decision tree, it is possible to distinguish between points of decision and points where chance and probability (uncertainty) may come into play. For example, this process can be used to illustrate possible returns from drilling a well and then exploiting a gas field.

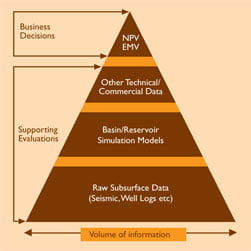

The diagram shows how inputs from geologists, engineers and others underpin the economic analysis and ultimately the calculation of value. These inputs relate to both internal and external data:

- Internal – technical data – relating to the costs involved in developing the block, e.g. the costs of building and developing the gas platforms, likely volume and quality of hydrocarbons.

- External – commercial data – about the future demand for, and price of, gas as well as likely tax changes, and information about local markets and other data.

Economists can then develop models projecting the likely costs and revenuesof developing new fields.

Essential components of these models are:

- revenues (price x volume)

- costs

- government take (e.g. taxes because the blocks that companies bid for are government property).Revenues less costs, less government take = the net cashflows which are discounted to give the NPV.

BG Group then uses all of this information to calculate the EMV of decisions. The EMV is equal to:

EMV = (NPV of success x chance of success) plus (NPV of failure x chance of failure)

The following example uses estimated returns expected from BG Group committing itself to drilling one exploration well. The net present cost will be £16m. There is a 16% chance that the three year project will be a success, yielding a return at NPV of £114m.

- First of all we work forward across the diagram from the decision fork where the choice is: ‘drill exploration well’ or ‘don’t drill exploration well’.

- Next, we set out the probabilities of gas being discovered and the NPV of success or failure (these are based on the geologists’ and economists’ calculations).

- If the well is not drilled there will be a return of £0. If the exploration well is drilled and no gas is found there will be a loss of £16m. There is an 84% chance of this being the case.

- If the exploration well is drilled and gas is found there will be a gain of £114m. There is a 16% chance of this happening.

We can now work out the EMV if the decision is made to go ahead with exploiting the field.

Therefore, on a risked basis drilling the well is attractive on economic grounds in that it generates a positive EMV. The opportunity would be presented to management to compete for funds in the capital allocation process.

Portfolio considerations

At this phase of the investment decision, a number of factors must be considered. The overriding goal of the company is to create shareholder value.

In order to achieve optimal growth for an acceptable level of risk, the company invests on a portfolio basis. This means that it will invest in a number of different wells and at times share the costs and working interests with partners in order to improve the risk/reward balance and stay within a budget.

Because the returns of these individual wells are likely to be uncorrelated or weakly correlated (e.g. failure in one exploration well is unlikely to affect the chance of success of another) the risk of the overall portfolio is lower than that of an individual well. This is especially important at the exploration stage due to the high risk of failure.

In addition to this idea of investing in projects which help to reduce the overall risk profile of the Company, decision makers must consider the strategic fit to the current business and where the company’s skills and expertise lie. Only after considering all of these factors can a decision be made on whether on not to invest in a particular project.

Conclusion

The gas market is an exciting one to be involved in. The world’s demand for energy is growing rapidly and it is imperative that it is supplied with clean energy reserves by principled companies.

BG Group is a major world player in this market and it constantly needs to make the right sorts of investment decisions which balance the needs of global consumers, its shareholders, the communities in which it operates, governments and other stakeholders.