A business aims to generate value for its owners, customers and other stakeholders. It must decide how to combine valuable resources – typically buildings and equipment, materials, people and knowledge – in such a way that the value of the output exceeds the costs of the input.

As resources flow into or out of a business, information flows too. Much of this information leaves a footprint in the form of financial data as the activities along with a business’ value chain result in financial outcomes. These are reported in financial statements including the cash flow and income statements as well as the formal balance sheet. Traditional accounting is concerned with reporting on a business in financial terms about its past performance.

Management accountants

Management accountants go beyond this to prepare both financial and non-financial information to support the business. They combine the relevant expertise of a traditional professionally qualified accountant with an understanding of the drivers of cost, risk and value in a business. This enables them to provide analysis and insights which are used to improve future performance.

CIMA, the Chartered Institute of Management Accountants, is the world’s leading professional body of management accountants. CIMA trained management accountants help to lead the process of strategy formation in a business. Strategy is the plan for achieving objectives. However, the strategy only points the way. Many decisions – large and small – must be made. Management is all about decision making and management accountants play a vital role in providing the crucial evidence that helps managers to make the right decisions.

Detecting, monitoring and evaluating risk is a very important element of this process. Management accountants use their accounting know-how to factor risk into decisions to help senior managers make realistic plans. The effectiveness of this depends on good communication. Even the best information has little value if not received by the right staff in the right format at the right time.

Types of decisions

A business continually makes decisions at all levels. Think of a retailer such as Next. To keep the brand’s high profile position, its managers have to make many decisions. Each major strategic decision leads to tactical decisions, which break down into operational decisions.

Decisions are broadly taken at three levels:

- Strategic decisions are big choices of identity and direction. Who are we? Where are we heading? These decisions are often complex and multi-dimensional. They may involve large sums of money, have a long-term impact and are usually taken by senior management.

- Tactical decisions are about how to manage performance to achieve the strategy. What resources are needed? What is the timescale? These decisions are distinctive but within clearer boundaries. They may involve significant resources, have medium-term implications and may be taken by senior or middle managers.

- Operational decisions are more routine and follow known rules. How many? To what specification? These decisions involve more limited resources, have a shorter-term application and can be taken by middle or first line managers.

Decisions in action

Imagine Next is planning to expand its product range. Its decisions would involve all three levels. All decisions depend on information. The key is to get the right information to the right people at the right time. For example, management accountants at Shell, the global oil and gas company, have been improving the way the company deals with the strategic and operational data about its global energy projects to improve strategic planning.

The company brought together data from 1200 projects and opportunities across 40 countries into a single system. Bringing the information together was a complex task due to the size of the company’s operations. However, the system has helped to define strategies and provide greater insight and detail to the Executive Committee and Board. This has given greater clarity on the business’s current and potential performance and highlighted where the company should allocate resources. To date, the system has helped Shell to increase its net present value by over 15%.

How are decisions made?

Management accountants use their skills alongside hard information to support decision making. Through intelligent analysis of information, they can generate alternative solutions and match these to the larger strategy. Each alternative can then be evaluated for its contribution towards objectives, taking into account:

- the timescale: money received in the future being worth less than money received today

- the risk: factoring in the probability of under or over-performance (also called negative or positive variance).

Once a decision is made and implemented it needs careful monitoring to ensure it keeps on track and any problems are detected early.

Reducing costs

The Electricity Supply Board (ESB) in Ireland faced the challenge of reducing its costs from £250m to £200m over five years. A team including management accountants was formed to break down costs and identify waste. The team discovered that ESB was carrying the costs of electrical faults caused by external building and construction companies. Meanwhile, the ESB technicians were over-burdened with paperwork. The team simplified and centralised this within a designated administration team. This meant the technical staff had more time to give a faster, flexible response to faults and to diagnose their causes. Major savings followed as faults plummeted by 75% and cost-efficiency at the company’s call centre significantly improved.

Some operational decisions can be made mainly from experience and based on an assessment of circumstances. More complex decisions need a systematic and structured approach. This is where decision-making models help.

Decision trees

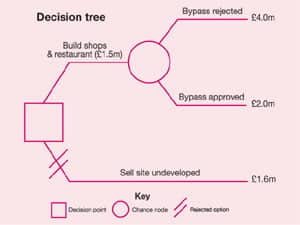

A decision tree is an outcome and probability map of the scenario. Most business problems may potentially have more than one solution. Each choice can lead to varying outcomes, some more likely than others.

To illustrate this, consider the decision faced by Prospect plc, a (fictitious) property development business. The company owns a town centre building site. This could be sold now for an estimated £1.6m. Alternatively, the site could be developed with shops and a restaurant at a cost of £1.5m. The property could then be sold for £4m – provided that a bypass proposal is rejected by the local council. The odds of the bypass being rejected are judged at about 75:25 due to environmental objections. If, however, the bypass were to be built, much tourist trade would be lost and the value of the development would only be £2m. Which choice should Prospect plc make? A decision tree is a useful tool when analysing choices of this kind.

Possible outcomes

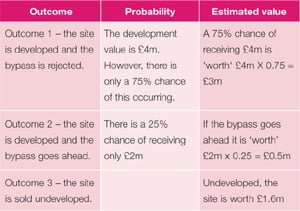

There are three possible outcomes to this scenario, each of which can be given a financial value.

To calculate the possible yield of developing the site, the values of outcomes 1 and 2 are combined. The cost of development is then subtracted: £3m + £0.5m – £1.5m = £2m

This compares to the value of selling the undeveloped site at only £1.6m. On this basis, depending on its attitude to risk and the likely timescales, the company is likely to build shops and restaurants.

Decision trees encourage managers to look at a range of options rather than relying on ‘gut feeling’. However, they are only as accurate as of the data on which they are based. This data is usually based on estimates. They do also run the risk of over-simplifying a problem, particularly where human or other external factors are involved. Other analysis tools can supplement the decision-making process.

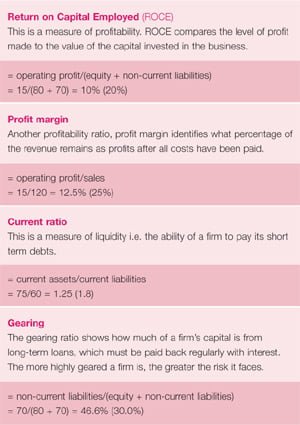

Ratio analysis

Businesses generate a huge amount of data. Management accountants can use a number of the company’s key accounting statements to extract greater meaning from this information.

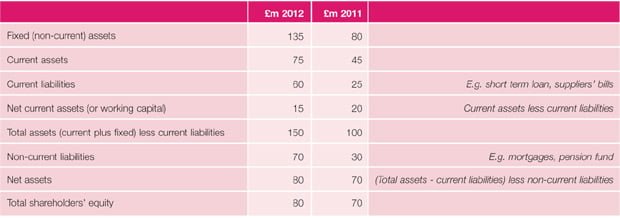

Prospect plc – Balance sheet/statement of financial position as of 31 March 2012

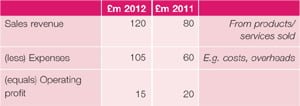

The income statement sets out the total sales revenue and subtracts the costs of generating that revenue to give operating profit. This is the surplus earned by the normal operations of the company and tells us the most about underlying business performance.

To continue to use the earlier illustrative example, Prospect plc is expanding rapidly as it builds a commercial property portfolio consisting mainly of shops and offices. The company receives rents and also benefits from any profits when it sells property and sites.

Prospect plc – Summarised income statement for the year ending 31 March 2012 (against previous year for comparison)

The balance sheet (or statement of financial position) shows the wealth of a company at a particular date. It lists the company’s assets (what it owns) followed by its liabilities (what it owes) – the difference being the net assets. Assets may be current, such as cash, or fixed, such as property or equipment. This value represents the shareholders’ equity – the value in the company that the shareholders actually own.

This looks as if Prospect plc has expanded very fast indeed – but how strong is its performance? Accounting ratios allow different pieces of financial data to be compared. Analysing some key ratios helps to explore behind the figures and offer strong clues for the business to steer towards its objectives (previous year data in brackets):

The chart shows every sign of a firm that has expanded too quickly:

- sales have increased by an impressive 50% in one year

- however, profitability has halved

- liquidity has weakened while gearing is more risky at nearly 50%.

The result is a danger signal! Management accountants investigate this sort of data in order to alert managers to worrying trends, as well as to possible opportunities.

Conclusion

Management accountants use complex business data to help businesses identify critical points and isolate weak and underperforming systems. It can also uncover opportunities that lie hidden under routines and processes.

CIMA trained management accountants work at all levels in a business and partner with managers across various business functions. This can become a real source of competitive advantage that is resistant to copying by competitors.